Mortgage Experience you can rely on

Trust us to help you find the right mortgage options and products for your current financial situation.

Mortgage financing can be confusing, it doesn't have to be, here's the plan.

Get started right away

The best place to start is to connect with us directly. The mortgage process is personal. Our commitment is to listen to all your needs, assess your financial situation, and provide you with a clear plan forward.

Get a clear plan

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming. Let us cut through the noise, we'll outline the best mortgage products available, with your needs in mind.

Let us handle the details

When it comes time to arranging your mortgage, we have the experience to bring it together. We'll make sure you know exactly where you stand at all times. No surprises. We've got you covered.

Let's run some numbers.

Start by telling us where you're at in your home buying journey.

Check Out Our Team

What people that work with us are saying

Home Buyers Tips

Everything you need, all in one place.

We can help you arrange mortgage financing for these services:

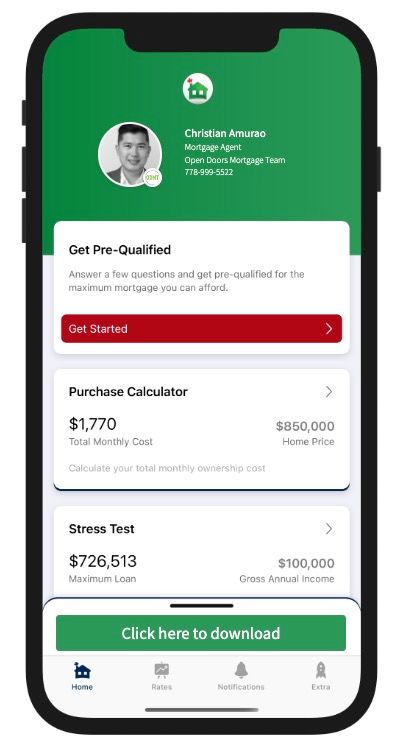

DOWNLOAD MY MORTGAGE TOOLBOX

WHAT YOU CAN DO WITH MY APP:

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

LET'S RUN SOME NUMBERS

OUR BLOG IS KEPT UP TO DATE SO YOU CAN STAY INFORMED!

Wondering If Now’s the Right Time to Buy a Home? Start With These Questions Instead. Whether you're looking to buy your first home, move into something bigger, downsize, or find that perfect place to retire, it’s normal to feel unsure—especially with all the noise in the news about the economy and the housing market. The truth is, even in the most stable times, predicting the “perfect” time to buy a home is incredibly hard. The market will always have its ups and downs, and the headlines will never give you the full story. So instead of trying to time the market, here’s a different approach: Focus on your personal readiness—because that’s what truly matters. Here are some key questions to reflect on that can help bring clarity: Would owning a home right now put me in a stronger financial position in the long run? Can I comfortably afford a mortgage while maintaining the lifestyle I want? Is my job or income stable enough to support a new home? Do I have enough saved for a down payment, closing costs, and a little buffer? How long do I plan to stay in the property? If I had to sell earlier than planned, would I be financially okay? Will buying a home now support my long-term goals? Am I ready because I want to buy, or because I feel pressure to act quickly? Am I hesitating because of market fears, or do I have legitimate concerns? These are personal questions, not market ones—and that’s the point. The economy might change tomorrow, but your answers today can guide you toward a decision that actually fits your life. Here’s How I Can Help Buying a home doesn’t have to be stressful when you have a plan and someone to guide you through it. If you want to explore your options, talk through your goals, or just get a better sense of what’s possible, I’m here to help. The best place to start? A mortgage pre-approval . It’s free, it doesn’t lock you into anything, and it gives you a clear picture of what you can afford—so you can move forward with confidence, whether that means buying now or waiting. You don’t have to figure this out alone. If you’re curious, let’s talk. Together, we can map out a homebuying plan that works for you.

Want a Better Credit Score? Here’s What Actually Works Your credit score plays a major role in your ability to qualify for a mortgage—and it directly affects the interest rates and products you’ll be offered. If your goal is to access the best mortgage options on the market, improving your credit is one of the smartest financial moves you can make. Here’s a breakdown of what truly matters—and what you can start doing today to build and maintain a strong credit profile. 1. Always Pay On Time Late payments are the fastest way to damage your credit score—and on-time payments are the most powerful way to boost it. When you borrow money, whether it’s a credit card, car loan, or mortgage, you agree to repay it on a schedule. If you stick to that agreement, lenders reward you with good credit. But if you fall behind, missed payments are reported to credit bureaus and your score takes a hit. A single missed payment over 30 days late can hurt your score. Missed payments beyond 120 days may go to collections—and collections stay on your report for up to six years . Quick tip: Lenders typically report missed payments only if they’re more than 30 days overdue. So if you miss a Friday payment and make it up on Monday, you're probably in the clear—but don't make it a habit. 2. Avoid Taking On Unnecessary Credit Once you have at least two active credit accounts (like a credit card and a car loan), it’s best to pause on applying for more—unless you truly need it. Every time a lender checks your credit, a “hard inquiry” appears on your report. Too many inquiries in a short time can bring your score down slightly. Better idea? If your current lender offers a credit limit increase , take it. Higher available credit (when used responsibly) actually improves your credit utilization ratio, which we’ll get into next. 3. Keep Credit Usage Low How much of your available credit you actually use—also known as credit utilization —is another major factor in your score. Here’s the sweet spot: Aim to use 15–25% of your limit if possible. Never exceed 60% , especially if you plan to apply for a mortgage soon. So, if your credit card limit is $5,000, try to keep your balance under $1,250—and pay it off in full each month. Maxing out your cards or carrying high balances (even if you make the minimum payment) can tank your score. 4. Monitor Your Credit Report About 1 in 5 credit reports contain errors. That’s not a small number—and even a minor mistake could cost you when it’s time to get approved for a mortgage. Check your report at least once a year (or sign up for a monitoring service). Look for: Incorrect balances Accounts you don’t recognize Missed payments you know were paid You can request reports directly from Equifax and TransUnion , Canada’s two national credit bureaus. If something looks off, dispute it right away. 5. Deal with Collections Fast If you spot an account in collections—don’t ignore it. Even small unpaid bills (a leftover phone bill, a missed utility payment) can drag down your score for years. Reach out to the creditor or collection agency and arrange payment as quickly as possible . Once settled, ask for written confirmation and ensure it’s updated on your credit report. 6. Use Your Credit—Don’t Just Hold It Credit cards won’t help your score if you’re not using them. Inactive cards may not report consistently to the credit bureaus—or worse, may be closed due to inactivity. Use your cards at least once every three months. Many people put routine expenses like groceries or gas on their cards and pay them off right away. It’s a simple way to show regular, responsible use. In Summary: Improving your credit score isn’t complicated, but it does take consistency: Pay everything on time Keep balances low Limit new credit applications Monitor your report and handle issues quickly Use your credit regularly Following these principles will steadily increase your creditworthiness—and bring you closer to qualifying for the best mortgage rates available. Ready to review your credit in more detail or start prepping for a mortgage? I’m here to help—reach out anytime!

Starting from Scratch: How to Build Credit the Smart Way If you're just beginning your personal finance journey and wondering how to build credit from the ground up, you're not alone. Many people find themselves stuck in the classic credit paradox: you need credit to build a credit history, but you can’t get credit without already having one. So, how do you break in? Let’s walk through the basics—step by step. Credit Building Isn’t Instant—Start Now First, understand this: building good credit is a marathon, not a sprint. For those planning to apply for a mortgage in the future, lenders typically want to see at least two active credit accounts (credit cards, personal loans, or lines of credit), each with a limit of $2,500 or more , and reporting positively for at least two years . If that sounds like a lot—it is. But everyone has to start somewhere, and the best time to begin is now. Step 1: Start with a Secured Credit Card When you're new to credit, traditional lenders often say “no” simply because there’s nothing in your file. That’s where a secured credit card comes in. Here’s how it works: You provide a deposit—say, $1,000—and that becomes your credit limit. Use the card for everyday purchases (groceries, phone bill, streaming services). Pay the balance off in full each month. Your activity is reported to the credit bureaus, and after a few months of on-time payments, you begin to establish a credit score. ✅ Pro tip: Before you apply, ask if the lender reports to both Equifax and TransUnion . If they don’t, your credit-building efforts won’t be reflected where it counts. Step 2: Move Toward an Unsecured Trade Line Once you’ve got a few months of solid payment history, you can apply for an unsecured credit card or a small personal loan. A car loan could also serve as a second trade line. Again, make sure the account reports to both credit bureaus, and always pay on time. At this point, your focus should be consistency and patience. Avoid maxing out your credit, and keep your utilization under 30% of your available limit. What If You Need a Mortgage Before Your Credit Is Ready? If homeownership is on the horizon but your credit history isn’t quite there yet, don’t panic. You still have a few options. One path is to apply with a co-signer —someone with strong credit and income who is willing to share the responsibility. The mortgage will be based on their credit profile, but your name will also be on the loan, helping you build a record of mortgage payments. Ideally, when the term is up and your credit has matured, you can refinance and qualify on your own. Start with a Plan—Stick to It Building credit may take a couple of years, but it all starts with a plan—and the right guidance. Whether you're figuring out your first steps or getting mortgage-ready, we’re here to help. Need advice on credit, mortgage options, or how to get started? Let’s talk.