Mortgage Experience you can rely on

Trust us to help you find the right mortgage options and products for your current financial situation.

Mortgage financing can be confusing, it doesn't have to be, here's the plan.

Get started right away

The best place to start is to connect with us directly. The mortgage process is personal. Our commitment is to listen to all your needs, assess your financial situation, and provide you with a clear plan forward.

Get a clear plan

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming. Let us cut through the noise, we'll outline the best mortgage products available, with your needs in mind.

Let us handle the details

When it comes time to arranging your mortgage, we have the experience to bring it together. We'll make sure you know exactly where you stand at all times. No surprises. We've got you covered.

Let's run some numbers.

Start by telling us where you're at in your home buying journey.

Check Out Our Team

What people that work with us are saying

Home Buyers Tips

Everything you need, all in one place.

We can help you arrange mortgage financing for these services:

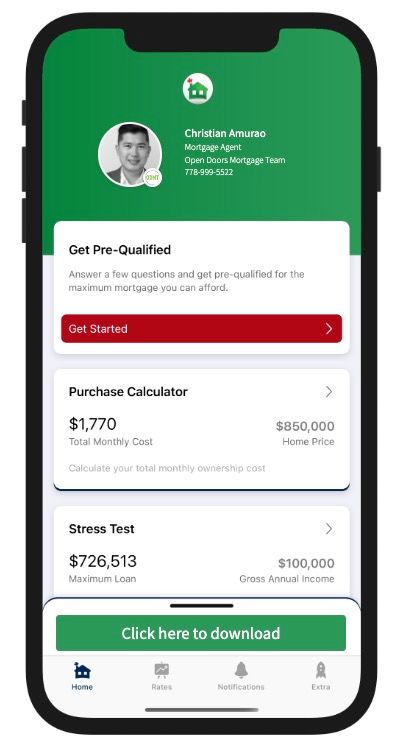

DOWNLOAD MY MORTGAGE TOOLBOX

WHAT YOU CAN DO WITH MY APP:

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

LET'S RUN SOME NUMBERS

OUR BLOG IS KEPT UP TO DATE SO YOU CAN STAY INFORMED!

Starting from Scratch: How to Build Credit the Smart Way If you're just beginning your personal finance journey and wondering how to build credit from the ground up, you're not alone. Many people find themselves stuck in the classic credit paradox: you need credit to build a credit history, but you can’t get credit without already having one. So, how do you break in? Let’s walk through the basics—step by step. Credit Building Isn’t Instant—Start Now First, understand this: building good credit is a marathon, not a sprint. For those planning to apply for a mortgage in the future, lenders typically want to see at least two active credit accounts (credit cards, personal loans, or lines of credit), each with a limit of $2,500 or more , and reporting positively for at least two years . If that sounds like a lot—it is. But everyone has to start somewhere, and the best time to begin is now. Step 1: Start with a Secured Credit Card When you're new to credit, traditional lenders often say “no” simply because there’s nothing in your file. That’s where a secured credit card comes in. Here’s how it works: You provide a deposit—say, $1,000—and that becomes your credit limit. Use the card for everyday purchases (groceries, phone bill, streaming services). Pay the balance off in full each month. Your activity is reported to the credit bureaus, and after a few months of on-time payments, you begin to establish a credit score. ✅ Pro tip: Before you apply, ask if the lender reports to both Equifax and TransUnion . If they don’t, your credit-building efforts won’t be reflected where it counts. Step 2: Move Toward an Unsecured Trade Line Once you’ve got a few months of solid payment history, you can apply for an unsecured credit card or a small personal loan. A car loan could also serve as a second trade line. Again, make sure the account reports to both credit bureaus, and always pay on time. At this point, your focus should be consistency and patience. Avoid maxing out your credit, and keep your utilization under 30% of your available limit. What If You Need a Mortgage Before Your Credit Is Ready? If homeownership is on the horizon but your credit history isn’t quite there yet, don’t panic. You still have a few options. One path is to apply with a co-signer —someone with strong credit and income who is willing to share the responsibility. The mortgage will be based on their credit profile, but your name will also be on the loan, helping you build a record of mortgage payments. Ideally, when the term is up and your credit has matured, you can refinance and qualify on your own. Start with a Plan—Stick to It Building credit may take a couple of years, but it all starts with a plan—and the right guidance. Whether you're figuring out your first steps or getting mortgage-ready, we’re here to help. Need advice on credit, mortgage options, or how to get started? Let’s talk.

Need to Free Up Some Cash? Your Home Equity Could Help If you've owned your home for a while, chances are it’s gone up in value. That increase—paired with what you’ve already paid down—is called home equity, and it’s one of the biggest financial advantages of owning property. Still, many Canadians don’t realize they can tap into that equity to improve their financial flexibility, fund major expenses, or support life goals—all without selling their home. Let’s break down what home equity is and how you might be able to use it to your advantage. First, What Is Home Equity? Home equity is the difference between what your home is worth and what you still owe on it. Example: If your home is valued at $700,000 and you owe $200,000 on your mortgage, you have $500,000 in equity . That’s real financial power—and depending on your situation, there are a few smart ways to access it. Option 1: Refinance Your Mortgage A traditional mortgage refinance is one of the most common ways to tap into your home’s equity. If you qualify, you can borrow up to 80% of your home’s appraised value , minus what you still owe. Example: Your home is worth $600,000 You owe $350,000 You can refinance up to $480,000 (80% of $600K) That gives you access to $130,000 in equity You’ll pay off your existing mortgage and take the difference as a lump sum, which you can use however you choose—renovations, investments, debt consolidation, or even a well-earned vacation. Even if your mortgage is fully paid off, you can still refinance and borrow against your home’s value. Option 2: Consider a Reverse Mortgage (Ages 55+) If you're 55 or older, a reverse mortgage could be a flexible way to access tax-free cash from your home—without needing to make monthly payments. You keep full ownership of your home, and the loan only becomes repayable when you sell, move out, or pass away. While you won’t be able to borrow as much as a conventional refinance (the exact amount depends on your age and property value), this option offers freedom and peace of mind—especially for retirees who are equity-rich but cash-flow tight. Reverse mortgage rates are typically a bit higher than traditional mortgages, but you won’t need to pass income or credit checks to qualify. Option 3: Open a Home Equity Line of Credit (HELOC) Think of a HELOC as a reusable credit line backed by your home. You get approved for a set amount, and only pay interest on what you actually use. Need $10,000 for a new roof? Use the line. Don’t need anything for six months? No payments required. HELOCs offer flexibility and low interest rates compared to personal loans or credit cards. But they can be harder to qualify for and typically require strong credit, stable income, and a solid debt ratio. Option 4: Get a Second Mortgage Let’s say you’re mid-term on your current mortgage and breaking it would mean hefty penalties. A second mortgage could be a temporary solution. It allows you to borrow a lump sum against your home’s equity, without touching your existing mortgage. Second mortgages usually come with higher interest rates and shorter terms, so they’re best suited for short-term needs like bridging a gap, paying off urgent debt, or funding a one-time project. So, What’s Right for You? There’s no one-size-fits-all solution. The right option depends on your financial goals, your current mortgage, your credit, and how much equity you have available. We’re here to walk you through your choices and help you find a strategy that works best for your situation. Ready to explore your options? Let’s talk about how your home’s equity could be working harder for you. No pressure, no obligation—just solid advice.

How to Start Saving for a Down Payment (Without Overhauling Your Life) Let’s face it—saving money isn’t always easy. Life is expensive, and setting aside extra cash takes discipline and a clear plan. Whether your goal is to buy your first home or make a move to something new, building up a down payment is one of the biggest financial hurdles. The good news? You don’t have to do it alone—and it might be simpler than you think. Step 1: Know Your Numbers Before you can start saving, you need to know where you stand. That means getting clear on two things: how much money you bring in and how much of it is going out. Figure out your monthly income. Use your net (after-tax) income, not your gross. If you’re self-employed or your income fluctuates, take an average over the last few months. Don’t forget to include occasional income like tax returns, bonuses, or government benefits. Track your spending. Go through your last 2–3 months of bank and credit card statements. List out your regular bills (rent, phone, groceries), then your extras (dining out, subscriptions, impulse buys). You might be surprised where your money’s going. This part isn’t always fun—but it’s empowering. You can’t change what you don’t see. Step 2: Create a Plan That Works for You Once you have the full picture, it’s time to make a plan. The basic formula for saving is simple: Spend less than you earn. Save the difference. But in real life, it’s more about small adjustments than major sacrifices. Cut what doesn’t matter. Cancel unused subscriptions or set a dining-out limit. Automate your savings. Set up a separate “down payment” account and auto-transfer money on payday—even if it’s just $50. Find ways to boost your income. Can you pick up a side job, sell unused stuff, or ask for a raise? Consistency matters more than big chunks. Start small and build momentum. Step 3: Think Bigger Than Just Saving A lot of people assume saving for a down payment is the first—and only—step toward buying a home. But there’s more to it. When you apply for a mortgage, lenders look at: Your income Your debt Your credit score Your down payment That means even while you’re saving, you can (and should) be doing things like: Building your credit score Paying down high-interest debt Gathering documents for pre-approval That’s where we come in. Step 4: Get Advice Early Saving up for a home doesn’t have to be a solo mission. In fact, talking to a mortgage professional early in the process can help you avoid missteps and reach your goal faster. We can: Help you calculate how much you actually need to save Offer tips to strengthen your application while you save Explore alternate down payment options (like gifts or programs for first-time buyers) Build a step-by-step plan to get you mortgage-ready Ready to get serious about buying a home? We’d love to help you build a plan that fits your life—and your goals. Reach out anytime for a no-pressure conversation.